Most North Georgia homeowners assume filing a storm damage claim is simple. It isn’t. Georgia law requires insurers to acknowledge your claim within 15 days, make a decision within 15 to 60 days, and issue approved payouts within 10 days. But many homeowners miss critical deadlines, skip key documentation steps, or accept the first offer without question. The result? Thousands of dollars left on the table. This guide walks you through every stage of the claims process, from understanding your policy to disputing a denial, so you can protect your home and your finances with confidence.

Table of Contents

- Understanding your policy and storm coverage

- Step-by-step: Filing a storm damage claim in Georgia

- Navigating adjusters, denials, and underpayment traps

- Financial realities: Deductibles, settlements, and recent Georgia regulations

- What most homeowners don’t realize about storm claims in Georgia

- Next steps: Fix your storm-damaged roof with local help

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Know your deadlines | Georgia requires fast claim filing and has strict insurer response deadlines. |

| Understand deductibles | Storm deductibles can be a large upfront cost—typically $3,000 to $15,000 for most homes. |

| Document everything | Photos, repair estimates, and storm reports are critical for successful claims and appeals. |

| Expect negotiation | Insurer underpayment is common; get expert help or a public adjuster if needed. |

| Stay updated on laws | New Georgia laws and savings options can help reduce your out-of-pocket costs in 2026 and beyond. |

Understanding your policy and storm coverage

To understand how the claims process unfolds, you first need to know what’s actually covered under your policy. Most Georgia homeowners have standard HO-3 policies, but the fine print varies a lot. Knowing your coverage before a storm hits can mean the difference between a full payout and a frustrating denial.

Key coverage types to review:

- Wind and hail deductibles: In Georgia, wind and hail deductibles are typically 1 to 5% of your dwelling coverage with no annual cap. On a $300,000 home, that’s $3,000 to $15,000 out of pocket before insurance pays a dime.

- Wind-driven rain vs. flooding: Most policies cover damage from rain that enters through a wind-created opening. But if water enters through a door, window, or existing gap, it may be excluded. Flood damage requires a separate flood insurance policy entirely.

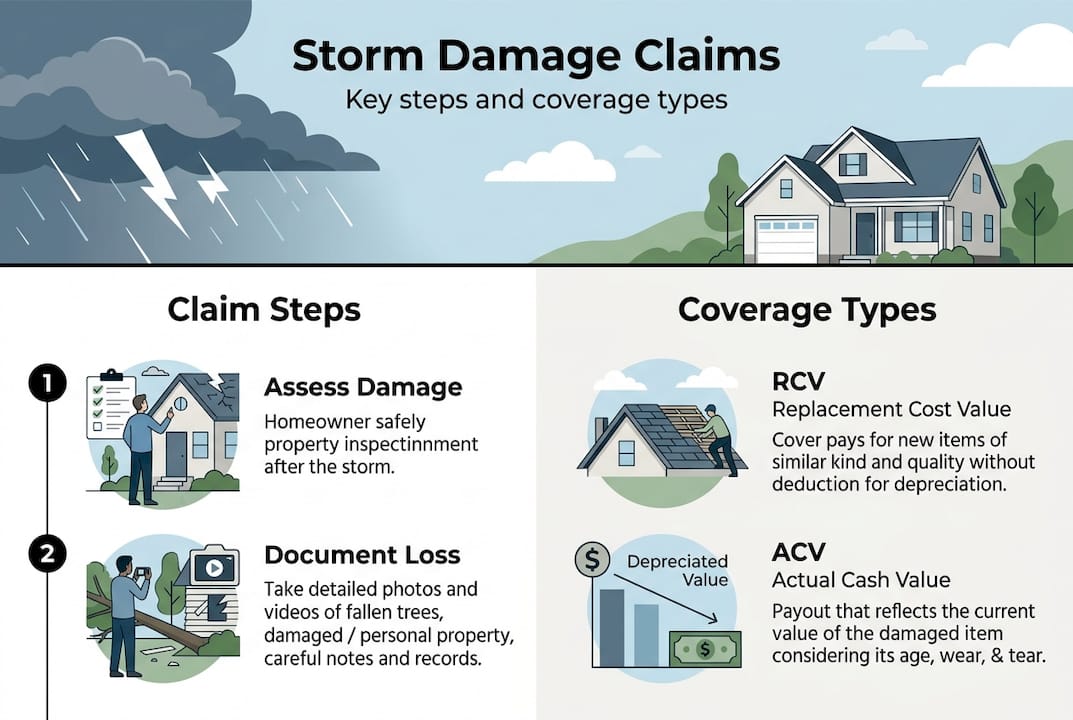

- RCV vs. ACV: Replacement Cost Value (RCV) pays what it costs to rebuild or replace your roof today. Actual Cash Value (ACV) subtracts depreciation. A 15-year-old roof on an ACV policy could yield a fraction of what a new roof costs.

- Ordinance & Law (O&L) coverage: When codes change, your insurer may not pay for required upgrades unless you have O&L coverage. Updates under the 2025 International Residential Code, like drip edge requirements, can add real cost to a roof replacement.

| Coverage type | What it pays | What it misses |

|---|---|---|

| RCV | Full replacement cost | Nothing, if you rebuild |

| ACV | Depreciated value | Gap between ACV and new cost |

| O&L | Code upgrade costs | Not included without add-on |

| Flood rider | Flood water damage | Standard policies exclude floods |

Pro Tip: Pull your declarations page right now and look for your wind/hail deductible percentage and whether you have RCV or ACV. Many homeowners discover they have ACV only after a major loss.

For a broader look at what Georgia homeowners must know before a storm, review your coverage annually. And if you want to understand what a full roof restoration explained looks like after a loss, that context matters when talking to your adjuster. You can also learn more about insurance coverage details specific to Georgia storm scenarios.

Step-by-step: Filing a storm damage claim in Georgia

Once you know your coverages, here’s exactly how to file a claim and avoid costly missteps. The sequence matters. Skipping a step or doing things out of order can delay your payout or reduce it significantly.

1. Assess your property safely. Walk your property after the storm passes and look for visible damage: missing shingles, dented gutters, cracked siding, broken windows. Do not climb on your roof alone.

2. Document everything immediately. Take time-stamped photos and video of all damage, inside and out. Download the National Weather Service (NWS) storm report for your area and date. This serves as independent evidence the storm occurred.

3. Contact your insurer quickly. You have up to one year to file, but file within 72 hours to 14 days of the storm for the fastest and strongest results. The sooner you file, the fresher the evidence.

4. Make temporary repairs only. Tarp over exposed areas to prevent further water damage. Keep every receipt. Avoid permanent repairs before the insurance adjuster inspects your home, or you may invalidate part of your claim.

5. Meet with the adjuster. Be present during the inspection. Walk them through all damage you documented. Do not assume they will find everything on their own.

6. Get your own estimate. Hire a trusted local roofing contractor to provide an independent repair estimate before accepting any settlement.

| Timeline milestone | Ideal timing |

|---|---|

| Document damage | Same day as storm |

| File your claim | Within 72 hours to 14 days |

| Adjuster inspection | Within 1 to 2 weeks of filing |

| Settlement decision | Within 15 to 60 days by Georgia law |

| Payment issued | Within 10 days of approval |

“Keep receipts for every temporary repair. These costs are typically reimbursable under your policy, and they protect you from additional damage liability.”

Pro Tip: Request the NWS storm data report for your zip code on the date of the storm. It’s free, official, and carries significant weight if your insurer tries to question whether damage-level winds or hail actually occurred.

For a detailed walkthrough of what comes next, visit our guide on roof repair after storm steps. It’s also worth reviewing gutter cleaning after storms, since clogged gutters are often flagged during inspections. And for the full picture on Georgia tornado insurance rules, that resource covers state-specific nuances.

Navigating adjusters, denials, and underpayment traps

Filing your claim is just the start. The outcome often depends on how you handle adjusters and disputes. Denials and underpayments are more common than most homeowners expect, and many go unchallenged simply because homeowners don’t know they have options.

Common reasons claims are denied or reduced:

- Wear and tear exclusion: Insurers may argue damage is due to age, not the storm.

- Missed hail bruises: Soft metal vents, flashing, and gutters often show hail impact that adjusters overlook.

- Lack of documentation: Gaps in photos or missing NWS reports weaken your case significantly.

- Pre-existing damage: Any condition that existed before the storm can be used to reduce your payout.

The good news is that denials are not final. You can request a re-inspection, submit additional evidence, or escalate the dispute.

“Use NWS storm data and an independent roofing inspection to counter wear-and-tear denials. Missed hail bruises on soft metals are one of the most overlooked evidence sources in storm claims.”

If your settlement still falls short, consider hiring a licensed public adjuster. Public adjusters increase settlements by 300 to 1,271% compared to insurers’ initial offers. That’s not a typo. The difference between accepting the first offer and fighting back can be enormous.

Pro Tip: Always get a second opinion from a licensed local roofer before accepting any settlement. An experienced contractor can identify damage the adjuster missed and provide written documentation to support a higher claim.

For reliable support navigating this process, our team is ready to find storm repair help and guide you through inspection and documentation. You can also revisit the storm claim FAQ for quick answers. And for general Georgia-specific claim strategies, review the Georgia tornado claim tips resource.

Financial realities: Deductibles, settlements, and recent Georgia regulations

Even with a successful claim, understanding the money side and changing laws is key to protecting your finances. Storm-related costs in Georgia have risen sharply, and new legislation affects how you can plan for them.

What you need to know about costs and settlements:

- Wind and hail deductibles typically range from 1 to 5% of dwelling coverage, meaning $3,000 to $15,000 on a $300,000 home.

- Georgia homeowners insurance premiums have risen 48% since 2019, driven largely by storm frequency and severity.

- RCV settlements pay out in two stages: an initial ACV payment, then the “recoverable depreciation” once repairs are completed.

- O&L coverage adds a third layer, reimbursing costs tied to code-mandated upgrades during repairs.

| Settlement component | What it covers | When you receive it |

|---|---|---|

| ACV payment | Depreciated value of damage | After claim approval |

| Recoverable depreciation | Gap between ACV and full cost | After repairs are completed |

| O&L reimbursement | Code upgrade costs | After upgrade proof submitted |

New Georgia financial tools in 2026:

- The Georgia Catastrophe Savings Account allows homeowners to set aside tax-advantaged funds specifically for storm deductibles.

- HB511, effective in 2026, formalizes the rules for these accounts, giving homeowners a practical way to buffer against high out-of-pocket deductibles.

- Non-renewal rates are climbing across North Georgia as insurers reassess risk, making proactive financial planning more important than ever.

For context on roofing safety insights and how they relate to post-storm inspections, that’s worth a read. And don’t forget about gutter cleaning tips as part of your ongoing maintenance plan to reduce future claim triggers.

What most homeowners don’t realize about storm claims in Georgia

After helping North Georgia homeowners through dozens of storm seasons, we’ve seen the same costly mistakes repeat. The biggest one isn’t missing a deadline or filing the wrong form. It’s waiting too long to review your policy.

Most people look at their policy only after a storm. By then, it’s too late to add O&L coverage or switch from ACV to RCV. A single annual review can prevent a five-figure gap between what you expected and what you actually receive.

Documentation gaps are equally damaging. A missing photo, an undated receipt, or a failure to pull the NWS report can give adjusters enough room to cut your payout. Be methodical. Document more than you think you need to.

And if your claim is denied? Negotiate. Hire a public adjuster if the amount at stake justifies it. Most homeowners accept denial as final. It’s not.

Finally, rising storm frequency means more insurers are issuing non-renewals or tightening restrictions in high-risk areas. Stay ahead of that risk by reviewing your Georgia storm insurance guide and shopping your policy every one to two years.

Next steps: Fix your storm-damaged roof with local help

Armed with these insights, here’s how you can get professional support and protect your home for the next storm.

At Infinity Roofing GA, we’ve been helping North Georgia homeowners navigate storm damage and insurance claims since 2018. We’re licensed, insured, and local. Our team inspects your damage, documents everything thoroughly, and works directly with your insurer to support maximum coverage. Visit our storm damage repair services page to request a same-day inspection. For a step-by-step overview of the repair process, check out our full roof repair guide. And if your gutters took a hit, our local gutter services team is ready to help. We’re your neighbor. Let us handle the hard part.

Frequently asked questions

How quickly do I need to file a storm damage claim in Georgia?

You must file within one year, but filing within 72 hours to 14 days gives you the best chance at a fast, full payout while evidence is fresh.

What’s the typical deductible for storm damage claims in North Georgia?

Storm deductibles in Georgia are usually 1 to 5% of dwelling coverage, which translates to $3,000 to $15,000 on a $300,000 home.

What happens if my claim is denied or underpaid?

You can dispute the outcome by submitting NWS storm reports and an independent inspection. Hiring a public adjuster can increase your settlement by 300 to 1,271% compared to the initial offer.

Are code upgrades like drip edge covered in Georgia storm claims?

Yes, code upgrades required by law are covered if you carry Ordinance & Law coverage, which is a separate add-on most standard policies don’t include by default.

What financial options exist for large deductibles after a major storm?

Georgia’s Catastrophe Savings Account, formalized under HB511 in 2026, lets homeowners set aside tax-advantaged funds specifically to cover high storm deductibles.