Most homeowners in North Georgia think the biggest roofing risk is storm damage. The real risk? Hiring the wrong contractor. If a roofer gets injured on your property and they have no insurance, Georgia law can make you financially responsible for their medical bills, lost wages, and more. That’s not a worst-case scenario. It happens regularly, and it can wipe out savings fast. This article explains exactly what insured roofing means, what your legal exposure looks like when a contractor isn’t covered, and how to protect yourself before you sign anything.

Table of Contents

- What does it mean for a roofing company to be insured?

- The financial and legal risks of hiring an uninsured roofing contractor

- How insured roofing companies protect your investment and peace of mind

- What to check and ask before hiring a roofing company in North Georgia

- The truth most Georgia homeowners don’t realize about roofing insurance

- Get protected: Insured roofing and storm repair in North Georgia

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Insurance shifts liability | Hiring an insured company protects your finances if a worker is hurt or property is damaged during roofing. |

| Avoid costly legal surprises | Without insurance, homeowners can face six-figure liability for accidents and injuries under Georgia law. |

| Proof equals protection | Always request and verify your roofer’s insurance certificate before any work starts. |

| Insured contractors secure warranties | Leading roofing warranties and reputable manufacturers demand contractor insurance for coverage to apply. |

| Peace of mind for your home | Choosing an insured roofer simplifies claims, boosts property value, and supports a worry-free investment. |

What does it mean for a roofing company to be insured?

Now that you know homeowners can face unexpected risks, it’s important to define what “insured” really means in roofing. It is not just one policy. A properly insured roofing company carries multiple types of coverage, each protecting a different person or scenario.

General liability insurance covers property damage caused by the roofer’s work. For example, if a crew member drops a tool and cracks your skylight or damages a neighbor’s fence, general liability pays for the repair. Without it, you are either fighting to recover costs out of pocket or absorbing the loss yourself.

Workers’ compensation insurance covers the roofing crew if someone is injured on the job. A roofer falling off your roof is a genuine, common occurrence. Workers’ comp pays for their medical care and a portion of their lost income while they recover. If the roofer lacks this coverage, homeowners can be financially liable for those expenses directly.

Some roofers also carry commercial auto insurance (for their work trucks and equipment) and umbrella policies for additional protection on larger jobs.

Here is a quick breakdown of what every insured roofing company in North Georgia should carry:

- ✅ General liability insurance (minimum $1 million per occurrence)

- ✅ Workers’ compensation insurance for all employees

- ✅ Commercial vehicle insurance for company vehicles

- ✅ Umbrella or excess liability for high-value projects

- ✅ Subcontractor coverage if they use third-party crews

Georgia does not have a statewide law requiring roofers to carry liability insurance. That surprises a lot of people. But just because it is not legally required does not mean it is optional from a risk standpoint. Our Georgia roofing insurance basics guide covers how this plays out specifically in North Georgia counties where storm damage claims are frequent.

Pro Tip: Before any work starts, ask the contractor for a certificate of insurance (also called a COI). This is a one-page document that lists their insurance carrier, policy numbers, coverage types, and expiration dates. If a roofer refuses to provide one or says “trust me, we’re covered,” walk away. A legitimate company always has this document ready.

The certificate should list you, the homeowner, as an additional insured party. This means their policy covers incidents on your property. It is a simple step that adds a significant layer of protection.

The financial and legal risks of hiring an uninsured roofing contractor

Once you know what insurance covers, here’s why skipping it exposes you to substantial risks.

The numbers are not small. Workers’ comp claims can reach hundreds of thousands to millions of dollars for serious injuries. A single fall resulting in a spinal injury, surgery, and long-term rehabilitation easily crosses $500,000. If the roofer has no coverage, and Georgia courts determine you were acting as their employer, that bill lands on your doorstep.

Key liability fact: Injury claims from construction accidents, including roofing falls, can reach seven figures when medical costs, rehabilitation, lost income, and legal fees are combined. Homeowners who hire uninsured contractors often absorb these costs directly.

Georgia’s O.C.G.A. § 34-9 Workers’ Compensation Act is the legal framework that creates this exposure. Under Georgia law, if a contractor is deemed to be functioning under your direction or control, you may be treated as their employer, regardless of whether you signed a formal employment contract. This is especially relevant when homeowners hire individual roofers or small crews operating as sole proprietors without proper business coverage.

Here are the most common legal scenarios where homeowners get left holding the financial responsibility:

- Scenario 1: An uninsured roofer falls and breaks an arm. Their medical costs total $85,000. They sue you as the property owner.

- Scenario 2: An uninsured subcontractor damages a neighbor’s vehicle with falling debris. The neighbor files a claim against your homeowner’s policy.

- Scenario 3: The roofer’s crew damages your HVAC unit. With no liability policy, there is no coverage and the contractor disappears.

- Scenario 4: Vicarious liability under Georgia law applies when uninsured subs cause third-party injuries, putting you directly in the legal line of fire.

Understanding filing insurance claims after storm damage is already stressful. Adding liability exposure from an uninsured contractor makes the process far worse.

Here is a realistic cost comparison that shows why saving money upfront often costs far more later:

| Situation | Potential homeowner cost |

|---|---|

| Insured roofer, accident occurs | $0 (contractor’s insurance pays) |

| Uninsured roofer, minor injury | $20,000 to $80,000 |

| Uninsured roofer, major injury | $250,000 to $1,000,000+ |

| Property damage from uninsured crew | $5,000 to $50,000 out of pocket |

| Savings from hiring uninsured roofer | $200 to $800 (typical quote difference) |

The math is straightforward. For more on your rights and responsibilities, check out more on roofing laws in Georgia. Knowing the law before you hire is always the smarter move.

How insured roofing companies protect your investment and peace of mind

After seeing the risks, it is time to cover the positive safeguards insured professionals bring to your next roofing project.

When something goes wrong on a job site, and sometimes it does even with experienced crews, the process with an insured company is clean and straightforward. There is no arguing about who pays, no waiting on lawsuits to resolve, and no surprise bills arriving months later. The insurance takes over, and your role is minimal.

Here is exactly how a properly insured roofing company handles an incident on your property:

- Incident is reported immediately to their insurance carrier. You are notified promptly.

- An adjuster is assigned by the contractor’s insurance company to evaluate the claim.

- Liability is confirmed through the certificate of insurance and your additional insured status.

- Repairs or compensation are arranged by the insurer, often within days for property damage.

- You sign off once the resolution is complete. No courtrooms, no attorney fees.

This process works because the coverage is in place before the first shingle is touched. That is the key. You cannot add insurance after an incident occurs.

Beyond accident coverage, insurance directly supports the quality of your roofing materials. GAF, one of the leading roofing material manufacturers in North America, requires contractors to be insured before they qualify for premium warranty programs like the Golden Pledge or System Plus warranties. These warranties cover materials and workmanship for decades. If your roofer is not insured, they cannot offer you these warranties, and your investment has no long-term protection.

Pro Tip: Keep a physical and digital copy of your contractor’s certificate of insurance, along with your warranty documentation and project photos. Some warranty claims require proof that the installation was done by a licensed, insured contractor. Losing that paperwork can void your warranty years down the road when you need it most.

For North Georgia homeowners exploring residential roofing options, material choice matters. But the contractor’s credentials matter just as much. A premium shingle installed by an uninsured roofer gives you none of the long-term warranty benefits the manufacturer offers.

The resale value of your home also benefits from documented, insured work. Buyers and home inspectors increasingly ask for contractor credentials and proof of insurance during real estate transactions. A documented, warranted roof replacement adds measurable value and speeds up closing.

What to check and ask before hiring a roofing company in North Georgia

Having learned the advantages, make sure you know how to verify an insured company before your next project.

The most important thing you can do before signing any contract is to request documentation upfront. A confident, legitimate roofing company will hand it over without hesitation. Anyone who delays, deflects, or says “we’ll get that to you later” is a red flag.

Here is a practical checklist to use before you commit to any roofing contractor:

- Request their certificate of insurance and verify it is current. Check the expiration date carefully.

- Confirm coverage types: They need both general liability and workers’ compensation.

- Verify that you are listed as an additional insured party on their policy for your project.

- Check their license status with the Georgia Secretary of State or applicable county licensing board.

- Look up their reviews on Google and the Better Business Bureau. Look for patterns, not just star ratings.

- Ask about subcontractors: Do their subs carry their own insurance, or are they covered under the main contractor’s policy?

- Get everything in writing: Scope of work, materials, payment schedule, start and end dates, and warranty details.

Under Georgia law, homeowners can become employers of uninsured roofers in certain situations, making this checklist more than just good practice. It is self-defense.

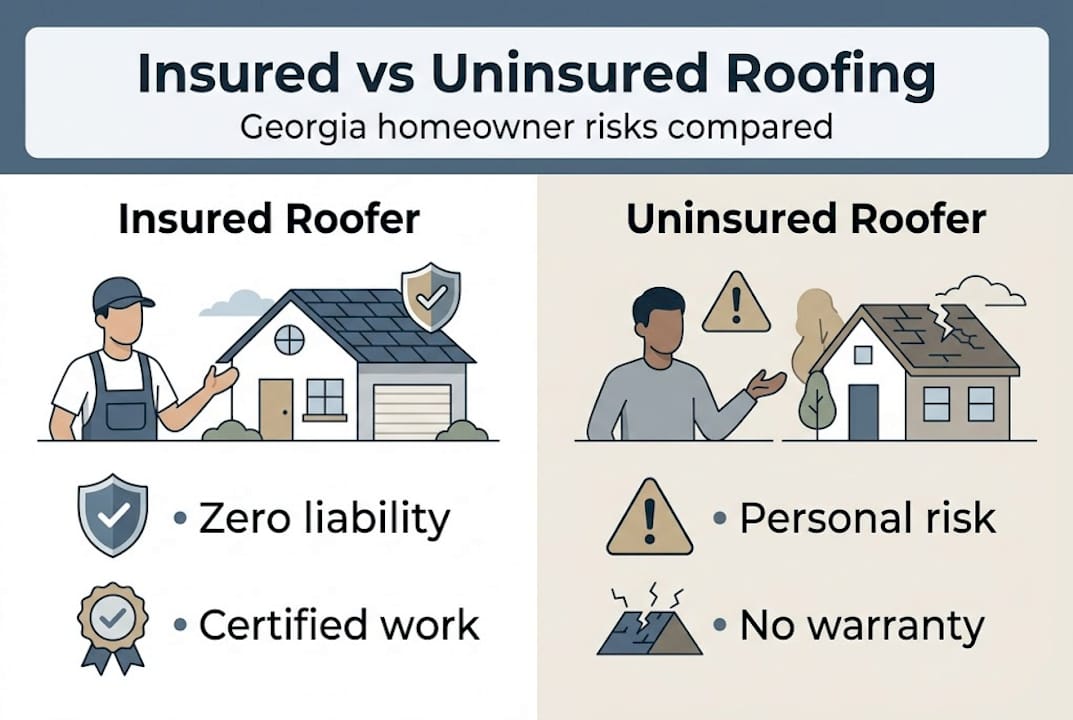

Here is a side-by-side look at what you get with each type of contractor:

| Factor | Insured roofing company | Uninsured roofing company |

|---|---|---|

| Accident liability | Covered by contractor’s policy | Falls on homeowner |

| Property damage coverage | Yes | No |

| Manufacturer warranty eligibility | Yes (GAF, Owens Corning, etc.) | Typically no |

| Workers’ comp coverage | Yes | No |

| Legal credibility | Fully documented | Limited or none |

| Typical price difference | Slightly higher | Lower upfront cost |

For a broader understanding, our roofing insurance guide breaks down how storm damage insurance works alongside contractor coverage in North Georgia. If you want to understand how safe job site practices factor into contractor selection, our roofing safety tips resource is a useful reference as well.

Red flags to watch for:

- Contractor only accepts cash

- No physical business address or local presence

- Pressures you to sign immediately after a storm (“storm chasers”)

- Cannot produce a COI within 24 hours

- No online reviews or recently created business profiles

- Offers a price that seems too far below every other quote

The truth most Georgia homeowners don’t realize about roofing insurance

Here is what most people miss in choosing an insured contractor, and what really matters for your protection.

Most homeowners assume that if something is not legally required, it is probably not that important. That assumption is dangerously wrong when it comes to roofing. Insurance is not a legal requirement in Georgia, but the absence of that legal mandate does not reduce your risk by a single dollar. If anything, the lack of a statewide requirement makes it easier for unqualified contractors to operate in our communities.

We have seen homeowners in the Dallas, Acworth, and Kennesaw areas sign contracts with out-of-state “storm chasers” who arrive after a bad hail event and disappear weeks later, taking deposits and leaving no warranty, no documentation, and no recourse. The legal system can pursue them, but practically, recovery is difficult and slow.

The real protection comes not from state mandates but from contractual standards. Manufacturers like GAF set their own requirements. Reputable insurance carriers set their own requirements. Home buyers and real estate attorneys increasingly set their own requirements. Meeting those standards is how a roofing company proves it is serious. It is how you know what you are getting for Georgia homeowners who want genuine protection and not just a lower quote.

Every reputable roofer in North Georgia should be able to prove their coverage in minutes. If they cannot, the savings are not worth it.

Get protected: Insured roofing and storm repair in North Georgia

Armed with this knowledge, taking action is easy. Here is how to get expert help and full protection in North Georgia.

At Infinity Roofing GA, we are fully licensed and insured, and we have been serving North Georgia homeowners since 2018. Whether you need storm damage assessment, a full roof replacement, or routine repairs, we bring complete documentation, premium materials, and manufacturer warranty eligibility to every job we do.

From storm damage repair to gutter services, we handle your project from start to finish with zero shortcuts. We provide our certificate of insurance upfront, assist with your insurance claim from start to finish, and back our work with warranties that hold up. Contact us today for a free inspection and same-day response. Protecting your home starts with choosing the right team.

Frequently asked questions

Is roofing insurance required by law in Georgia?

No, Georgia does not require roofing contractors to carry liability insurance statewide, but leading manufacturers and reputable warranty programs make it a firm requirement.

What could happen if I hire an uninsured roofer?

You could be held financially responsible for injuries or damages during the project. Homeowners can face liability for medical bills and damages that easily reach tens of thousands of dollars or more.

How do I verify my roofer’s insurance?

Ask for a certificate of insurance before work begins, then call their insurance carrier directly to confirm the policy is active and covers your type of project.

Does homeowner’s insurance cover accidents caused by uninsured roofers?

It depends on your policy. Many insurers exclude coverage for damages or injuries caused by uninsured contractors, which can leave you exposed to significant out-of-pocket costs.

Are insured roofing companies more expensive?

Insured roofers may charge slightly more, but that small difference protects you from potential liability that can reach hundreds of thousands of dollars in a worst-case scenario.