Most North Georgia homeowners believe a standard policy has them fully covered when a storm rolls through. That assumption can be very expensive. Standard homeowners insurance typically covers wind and hail damage but excludes flood damage entirely, which means ground-up flooding from heavy rain requires a completely separate policy. Add percentage-based deductibles that can run into thousands of dollars, and the real picture looks nothing like what most people expect. This guide walks you through what coverage actually means in North Georgia, where the gaps are, and how to protect your home and your finances before the next storm finds you unprepared.

Table of Contents

- What storm damage insurance really covers (and what it doesn’t)

- The hidden costs: Storm deductibles and out-of-pocket surprises

- Nuances and real examples: How claims are decided and common pitfalls

- Beyond payout: Why the right insurance and process speed your recovery

- Our take: Why going beyond minimum coverage is critical in storm-prone Georgia

- How we help North Georgia homeowners recover after a storm

- Frequently asked questions

Key Takeaways

| Point | Details |

|---|---|

| Not all storm damage is covered | While wind and hail are usually included, floods and long-term damage generally require separate policies or are excluded entirely. |

| Deductibles can add up | Wind/hail deductibles are often a percentage of your insured value, potentially costing thousands even with approved claims. |

| Details decide coverage | Timely documentation and insurer classification of damage—what caused it and whether it’s accidental—significantly influence insurance payouts. |

| Restoration is a process | Good insurance isn’t just about payment; it equips you for smoother repairs, compliance, and a quicker return to normal at home. |

| Expert help makes the difference | Experienced contractors, thorough records, and understanding policy nuances can help maximize both claim success and restoration speed. |

What storm damage insurance really covers (and what it doesn’t)

With misconceptions about coverage out of the way, let’s dig into the specifics of what a standard policy includes and where homeowners are most often left exposed.

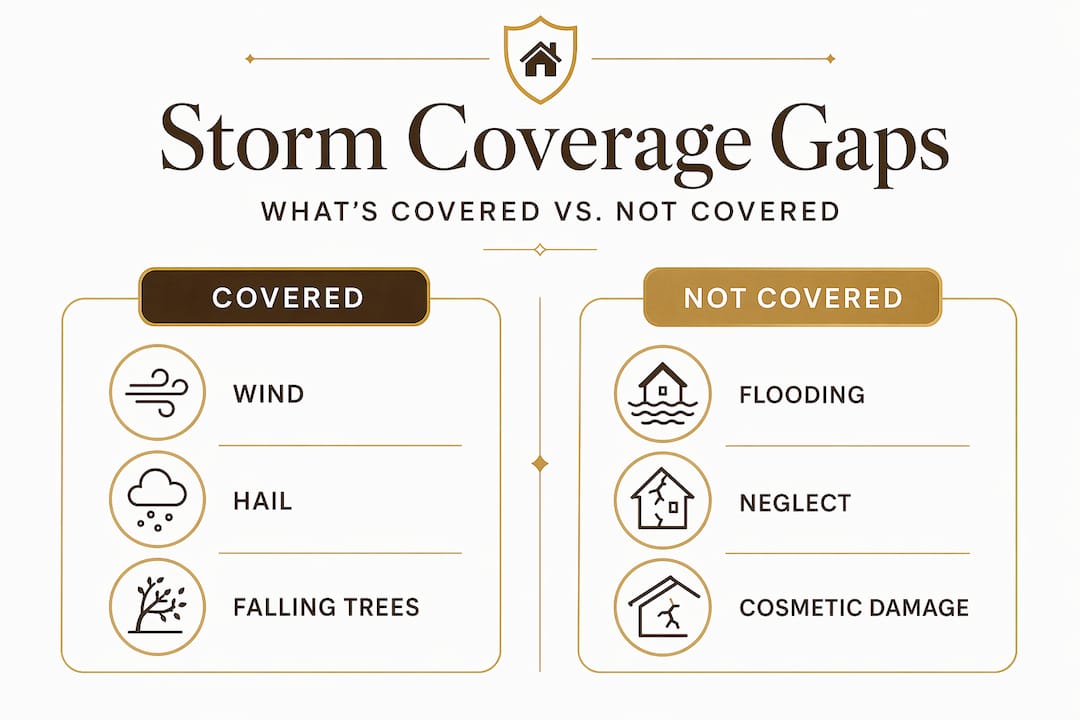

Covered perils: The basics

Most homeowners policies in Georgia cover what the industry calls “named perils.” Wind and hail sit at the top of that list. If a storm tears off shingles, snaps a tree limb onto your roof, or shatters a window with wind-driven debris, your policy will generally pay to repair the damage. Wind and hail coverage also usually extends to interior damage when water enters through a storm-created opening, such as a hole in the roof or a broken window.

That distinction matters more than most people realize. Rain that blows in through a storm-damaged roof is treated very differently from rain that overflows from a creek and floods your basement. One is typically covered. The other is almost never covered under a standard policy.

What is NOT covered

Flood damage is the biggest gap. Ground-up flooding, flash flooding, and storm surge are excluded from standard homeowners insurance across the board. If you want protection from those events, you need a separate flood insurance policy through the National Flood Insurance Program or a private carrier.

Beyond flooding, cosmetic damage, maintenance neglect, and gradual deterioration are also excluded. An adjuster who finds that your roof was already worn, curling, or missing granules before the storm will likely classify much of the damage as a maintenance issue rather than storm-related loss. That reclassification can dramatically reduce or eliminate your payout.

Here is a quick comparison so you can see the difference clearly:

| Type of damage | Typically covered? | Notes |

|---|---|---|

| Wind damage to roof | Yes | Sudden, storm-caused |

| Hail damage to shingles | Yes | Documented storm event required |

| Rain entering through storm opening | Usually yes | Must be tied to wind/hail damage |

| Ground-up flooding | No | Requires separate flood policy |

| Gradual roof deterioration | No | Classified as maintenance |

| Cosmetic damage only | Often excluded | Depends on policy language |

| Tree limb through roof | Yes | Sudden/accidental event |

Key exclusions to keep in mind:

- Flooding from any external water source (rivers, creeks, storm drains)

- Pre-existing wear and tear that the storm worsened

- Damage the insurer classifies as cosmetic, such as dented gutters with no functional impact

- Neglected maintenance, such as a roof that was already failing before the storm

Understanding the storm damage claims process and reviewing your roof insurance essentials before a storm hits puts you in a far stronger position when you need to file.

The hidden costs: Storm deductibles and out-of-pocket surprises

Now that you know what is covered and excluded, let us look at why storm claims can still result in substantial out-of-pocket costs even when your policy does apply.

Percentage-based deductibles are not what most people expect

Many North Georgia homeowners assume their deductible works like a car insurance deductible: a flat $1,000 or $2,000 fee. Wind and hail deductibles work differently. They are typically calculated as a percentage of your home’s total insured value.

Wind and hail deductibles commonly range from 1% to 5% of your home’s insured value. On a home insured for $350,000, that means your out-of-pocket cost before insurance pays a single dollar could be $3,500 at 1% or $17,500 at 5%. That is a major financial gap that catches homeowners completely off guard.

Here is a simple breakdown of how these numbers work:

| Home insured value | 1% deductible | 2% deductible | 3% deductible | 5% deductible |

|---|---|---|---|---|

| $200,000 | $2,000 | $4,000 | $6,000 | $10,000 |

| $300,000 | $3,000 | $6,000 | $9,000 | $15,000 |

| $350,000 | $3,500 | $7,000 | $10,500 | $17,500 |

| $500,000 | $5,000 | $10,000 | $15,000 | $25,000 |

Important: Flood damage from the ground up is not covered at all by a standard homeowners policy. No payout is possible without a separate flood insurance policy, regardless of how severe the damage is.

Pro Tip: Pull out your policy documents today and find the specific wind/hail deductible language. It may be listed separately from your standard deductible. Knowing that number now means no surprises later. Keep a dedicated savings fund to cover that amount, so you are not scrambling after a storm.

Getting solid roof insurance claim advice before you file helps you understand exactly what you owe out of pocket and what the insurance company is responsible for covering. That knowledge gives you leverage and confidence throughout the entire process.

Nuances and real examples: How claims are decided and common pitfalls

With these costs in mind, it is vital to understand how insurers determine what gets paid out and why two neighbors with nearly identical storm damage can walk away with very different claim results.

How adjusters classify your loss

When you file a claim, your insurer sends an adjuster to inspect the damage. That adjuster’s classification of the loss drives the entire outcome. If they label damage as sudden and accidental, caused directly by the storm, you are on track for a payout. If they classify it as cosmetic, maintenance-related, or gradual, that portion of the claim may be denied.

Rain infiltration through a damaged roof is a good example of where the line gets drawn carefully. If a hailstorm cracked your roof decking and rain came in through that opening, most policies will treat that as a covered event. But if the same storm pushed water through an existing crack that had been there for two seasons, the insurer can argue the real cause was deferred maintenance.

Timely documentation, insurer classification, and cause-of-loss are the three pillars that determine your claim’s outcome. Homeowners who understand this before they file move through the process much faster and with better results.

Step-by-step: What happens after storm damage

Following a clear process improves your odds significantly. Here is the order that matters most:

- Assess safety first. Do not enter damaged areas until you confirm there is no structural risk or live electrical hazard.

- Document everything immediately. Take photos and video of every visible impact point, from the roof and gutters to the yard and exterior walls. Time-stamp everything.

- Prevent further damage. Put a tarp over roof openings if safe to do so. Keep receipts for any temporary repairs. Insurers expect you to mitigate ongoing damage.

- Notify your insurer promptly. File your notice of loss as soon as possible. Delayed reporting can give the insurer grounds to question the timeline and severity of the damage.

- Cooperate fully during inspection. Be present during the adjuster visit and point out every area of concern. Do not assume they will find everything on their own.

- Get an independent contractor assessment. Having your own roofing contractor review the damage alongside the insurer’s adjuster is not just allowed, it is smart.

- Review the scope of loss carefully. Before repairs begin, confirm that the insurer’s scope of loss matches what your contractor documented.

Pro Tip: Create a dedicated folder, physical or digital, for every piece of storm-related documentation. That includes photos, weather reports confirming the storm date, repair estimates, and insurer correspondence. This single habit has helped many North Georgia homeowners avoid claim disputes.

Understanding how filing claims in Georgia works step by step keeps you from making the small process errors that delay payouts by weeks.

Beyond payout: Why the right insurance and process speed your recovery

Knowing how coverage nuances affect your claim, it is just as important to appreciate how your insurance shapes the entire restoration journey from the first assessment all the way through full repairs.

Coverage quality affects more than just the check you receive

A higher-quality policy with broader coverage, lower percentage deductibles, and strong replacement cost value provisions means your restoration can move faster and more completely. A bare-bones policy might technically cover the same storm event but leave you negotiating over scope for months.

The claims workflow includes documentation, insurer inspection, adjudication, scope-of-loss review, and permits before any physical repairs can begin. Each step requires clear cooperation between the homeowner, the insurer, and the roofing contractor. When documentation is incomplete or timelines are missed, that chain breaks down and your restoration drags on.

Why a qualified, licensed contractor is part of your insurance strategy

Here is something most homeowners do not think about: your roofing contractor is a key player in your insurance claim, not just in the repair work. An experienced, licensed contractor knows how to document storm damage in terms that align with how insurers evaluate scope of loss. They understand permit requirements, local building codes, and material standards that can affect whether the insurer approves the full replacement versus a patch.

Top reasons why timely, thorough insurance combined with a qualified contractor matters after a storm:

- Faster claim resolution because documentation is complete from the start

- Accurate scope of repairs that reflects actual storm damage rather than a minimized insurer estimate

- Permit coordination handled by professionals who know local North Georgia requirements

- Quality materials that meet insurer standards and protect your home long term

- Reduced risk of re-damage due to proper repair methods the first time around

Reviewing insurance claims step-by-step before you start and working with proven storm roof repair solutions ensures that the restoration process moves efficiently and that your home comes back to pre-storm condition correctly.

Our take: Why going beyond minimum coverage is critical in storm-prone Georgia

With the practical and financial realities explained, here is our candid perspective from years of working alongside North Georgia homeowners in the aftermath of severe storms.

We have seen the same scenario play out repeatedly. A homeowner files a claim after a significant storm feeling confident they are covered. Then the adjuster arrives and the conversation shifts. The insurer points to a high wind/hail deductible. They flag a section of the roof as pre-existing wear. They deny the gutter replacement as cosmetic. The homeowner leaves that conversation with a fraction of what they expected.

The real gap is not just in coverage. It is in preparation. Storm insurance and restoration are not simply about getting paid. Homeowners must navigate a claims workflow filled with classification decisions, documentation requirements, and coverage gaps that a basic policy does nothing to address. Most homeowners do not realize this until they are standing in front of a damaged home.

Our honest recommendation: review your policy annually with a licensed insurance professional who knows Georgia storm patterns. Understand your wind/hail deductible as a specific dollar amount, not just a percentage. Maintain your roof so that no adjuster can reasonably claim neglect. And when a storm does hit, partner with a contractor who has real experience handling insurance claims from start to finish.

Choosing insured roofers is not just about liability protection. It is about working with someone who can navigate the insurance process as effectively as they handle the physical repair work. That combination is what actually gets your home restored quickly and fully.

Going beyond the bare minimum in both coverage and contractor selection is not an upsell. In storm-prone North Georgia, it is simply the smart, responsible choice.

How we help North Georgia homeowners recover after a storm

If you are looking for real support when a storm hits and need to ensure your insurance and your restoration team are truly working for you, here is how we can help.

At Infinity Roofing GA, we have been working with North Georgia homeowners since 2018 to navigate storm damage repair and the insurance process that goes with it. We do not just fix roofs. We help you document damage accurately, communicate with your insurer, and make sure the scope of repairs reflects what actually happened to your home.

Our team handles everything from the initial damage assessment through final repairs, and we work directly with your insurance company throughout the process. Whether you need to review our storm damage repair services, want to understand home insurance roof repair better, or are still deciding between roof repair vs replacement, we have the resources and the experience to guide you clearly. Contact us today for a same-day response and a no-pressure assessment of your storm damage.

Frequently asked questions

Does homeowners insurance in North Georgia cover flood damage from a storm?

No, standard homeowners insurance excludes flood damage entirely. Homeowners need a separate flood policy for protection against ground-up or flash flooding, regardless of how the flood was triggered.

How do wind and hail deductibles affect a storm damage insurance claim?

Wind and hail deductibles typically range from 1% to 5% of your home’s insured value, meaning you could owe thousands of dollars out of pocket before your insurer pays anything on an approved claim.

What types of storm damage are typically not covered by insurance?

Ground-up flooding, maintenance neglect, and gradual deterioration are common exclusions from standard policies, along with purely cosmetic damage that does not affect the function of your roof or structure.

How can I improve my odds of a successful storm damage claim?

Fast, thorough documentation is the single biggest factor. Photograph damage immediately after the storm, keep all repair receipts, and cooperate fully and promptly during your insurer’s inspection to strengthen your claim.

Is wind-driven rain always covered by homeowners insurance?

If rain enters your home through a storm-created opening in your roof or windows, it is often covered as wind-driven damage. However, water that enters from overflowing creeks or rises from the ground is almost never covered under a standard policy.