Most homeowners assume their roof insurance deductible is a simple, flat dollar amount. It’s a reasonable assumption, but often wrong. Many policies carry separate wind and hail deductibles that are percentage-based, and on a $400,000 home, that 2% deductible means you owe $8,000 out of pocket before your insurer pays anything. Understanding what is insurance deductible for roofing, and how the different types work, is one of the most financially important things a homeowner can do before storm season arrives.

Table of Contents

- Key takeaways

- Types of roofing insurance deductibles

- Finding your deductible details in your policy

- Legal pitfalls and contractor deductible practices

- Practical steps before and after roof damage

- How deductibles affect repair vs. replacement decisions

- My take on roofing deductibles after years in this business

- How Ir-ga helps you navigate roofing claims with confidence

- FAQ

Key takeaways

| Point | Details |

|---|---|

| Two main deductible types | Roofing claims involve either flat dollar deductibles or percentage-based deductibles tied to your home’s insured value. |

| Wind and hail cost more | Separate wind/hail deductibles are commonly 1%–5% of dwelling coverage, far exceeding standard flat deductibles. |

| Read your declarations page | Your deductible type, amount, and trigger conditions are listed on the declarations page of your policy. |

| Contractors cannot waive deductibles | It is illegal in many states for roofers to pay or waive your deductible, and doing so can void your claim. |

| Prepare before storm season | Confirm your deductible types with your insurer every year and budget for percentage-based costs before damage occurs. |

Types of roofing insurance deductibles

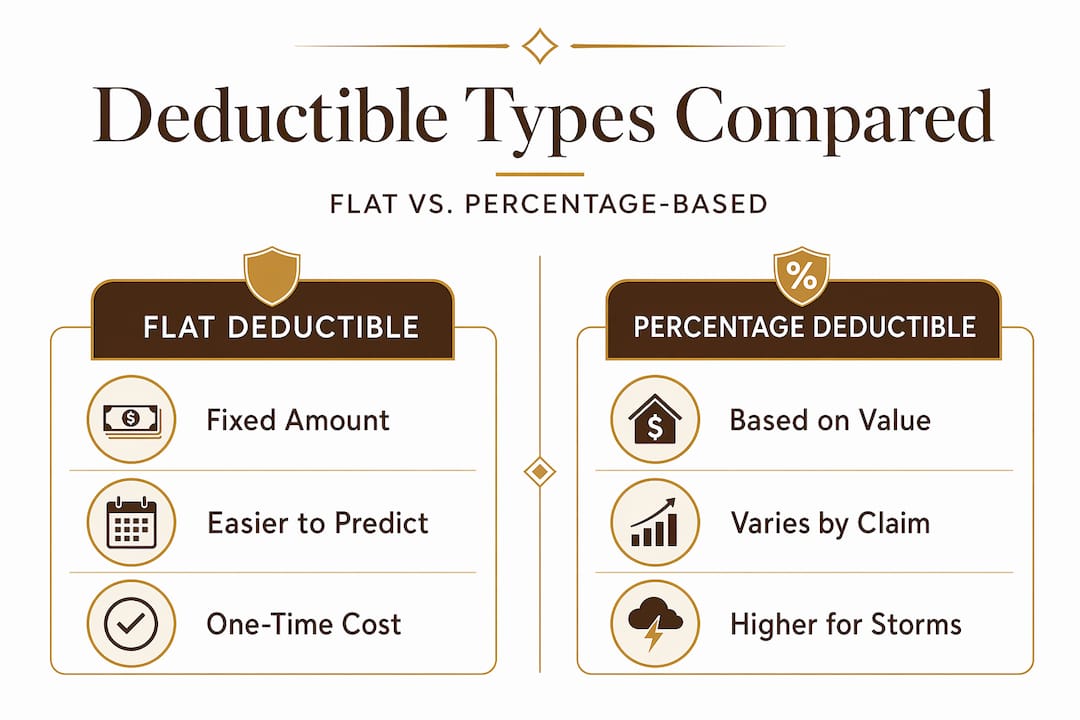

When homeowners ask what is insurance deductible for roofing, the answer starts with two core structures: flat deductibles and percentage deductibles.

Flat deductibles

A flat deductible is a fixed dollar amount that gets subtracted directly from your claim payout. Your insurer pays the difference. For example, if your roof sustains $10,000 in damage and you have a $500 deductible, your insurer pays $9,500. Flat deductibles are predictable and easy to budget for, which is why many homeowners prefer them.

Percentage deductibles

Percentage deductibles work differently. Instead of a set dollar amount, your deductible is calculated as a percentage of your home’s insured dwelling value, also called Coverage A. This structure is common for wind and hail damage, and the numbers can be significant.

Consider this: a 2% wind/hail deductible on a home insured for $400,000 means your out-of-pocket cost is $8,000 before any insurance money arrives. On a $420,000 home with a 2% deductible, what looked like a standard $2,500 deductible on paper becomes $8,400 out of pocket the moment hail damage is the trigger.

Here is a side-by-side look at how each type compares:

| Deductible type | How it’s calculated | Example (damage claim: $15,000) | Out-of-pocket cost |

|---|---|---|---|

| Flat deductible | Set dollar amount | $1,500 flat deductible | $1,500 |

| 1% percentage deductible | 1% of $350,000 dwelling coverage | Wind/hail trigger | $3,500 |

| 2% percentage deductible | 2% of $400,000 dwelling coverage | Wind/hail trigger | $8,000 |

| 5% percentage deductible | 5% of $300,000 dwelling coverage | Wind/hail trigger | $15,000 |

That last row is striking. A 5% deductible on a $300,000 home could mean your deductible equals the entire repair cost. This is not a theoretical scenario. It happens every storm season.

Pro Tip: Ask your insurance agent specifically whether your wind and hail deductible is separate from your standard deductible. Many homeowners discover this distinction only after filing a claim, when it’s too late to plan.

Many homeowners also mistakenly assume deductibles are flat rates, without realizing that wind and hail damage almost always triggers the higher percentage version. Knowing the difference before a storm hits puts you in a much stronger position.

Finding your deductible details in your policy

Your insurance policy holds all the answers. You just need to know where to look. The declarations page lists your deductible type and amount for each coverage line, including any separate wind or hail deductibles.

Here is what to look for when reviewing your declarations page:

- Standard deductible line: This shows your flat deductible for most covered perils, such as fire or theft.

- Wind/hail deductible line: This will show a percentage (such as “2% Wind/Hail Deductible”) or a separate flat amount specifically for those perils.

- Per occurrence vs. per policy term: Percentage deductibles commonly apply per occurrence, meaning each separate storm event triggers a new deductible. Two hailstorms in one year means you pay twice.

- Coverage A limit: This is your dwelling coverage amount and is the number used to calculate percentage-based deductibles. A higher Coverage A limit means a higher deductible dollar amount when percentage-based triggers apply.

Understanding how your dwelling coverage limit affects your deductible math is key. Insurers update Coverage A limits regularly to reflect inflation and rebuilding costs. Every time that number rises, your percentage-based deductible rises with it.

You can use the Ir-ga roof insurance claim guide to walk through exactly what to look for when reviewing your policy documents before filing a claim in North Georgia.

Pro Tip: Review your Coverage A limit every year at policy renewal. If it has risen significantly, recalculate what your wind/hail deductible would be in dollars. That number may surprise you, and adjusting your policy terms before a claim is far easier than dealing with the surprise after one.

Legal pitfalls and contractor deductible practices

This is where things get serious. One of the most common scams in the roofing industry involves contractors offering to “cover your deductible” or “work within your deductible.” It sounds helpful. It is actually illegal in many states, and it puts you at real financial and legal risk.

Texas law explicitly prohibits roofing contractors from paying, waiving, or absorbing a homeowner’s insurance deductible. Similar prohibitions exist across other states. When a contractor offers to eat your deductible, they are often inflating the claim amount to cover that cost, which is insurance fraud. If your insurer discovers this, your claim can be denied entirely. You could also face legal consequences as a policyholder, even if you did not initiate the arrangement.

Here is how to protect yourself when evaluating roofing contractors:

- Avoid anyone who leads with deductible waiving. Legitimate roofers do not make this offer.

- Get written, itemized estimates. This makes it easier to verify that the claim amount reflects actual damages and costs.

- Verify licensing and insurance. A licensed, insured contractor has too much to lose to engage in fraudulent billing practices.

- Check reviews and references. Complaints about inflated estimates or insurance disputes are red flags worth researching.

- Ask directly whether they handle insurance claims honestly. Trustworthy contractors welcome the question.

Choosing an insured, licensed roofer is one of the most important decisions you make after storm damage. It keeps your claim valid and your roof repair fully covered.

Pro Tip: If a contractor’s bid seems unusually low and they hint that they “take care of” your deductible, walk away. The short-term savings are not worth a denied claim or an insurance fraud investigation.

Practical steps before and after roof damage

Being prepared before a storm is the difference between a smooth claim and a financial scramble. Here is a straightforward process to follow:

- Review your policy now. Pull out your declarations page and confirm both your standard deductible and your wind/hail deductible. Note whether it is flat or percentage-based.

- Calculate your worst-case cost. Multiply your Coverage A limit by the wind/hail deductible percentage. That is the dollar amount you need to have available if a major storm strikes.

- Ask your insurer what triggers apply. Confirm with your agent which perils activate the percentage deductible versus the standard deductible. Confirming which deductible triggers apply to wind and hail helps you avoid costly surprises.

- Document your roof’s current condition. Take dated photos of your roof before storm season. This establishes a clear baseline if you need to prove damage occurred during a specific event.

- File your claim promptly after damage. Contact your insurer as soon as possible after a storm. Delayed reporting can complicate your claim.

- Get a licensed contractor involved early. A contractor experienced with storm damage insurance claims can help document damage accurately and support your claim without inflating costs.

- Keep all receipts and correspondence. Every phone call, email, and repair estimate related to your claim should be saved. This documentation protects you if disputes arise.

How deductibles affect repair vs. replacement decisions

Understanding your deductible structure directly shapes whether repairing or replacing your roof makes financial sense. This is where roof claim deductible details move from abstract policy language to real dollar decisions.

When repairs make sense

If you have a flat $1,000 deductible and face $4,000 in localized storm damage, filing a claim and covering your deductible leaves your insurer paying $3,000. That math works. But if your wind/hail deductible is 2% on a $350,000 home, your deductible is $7,000. For a $4,000 repair, filing the claim makes no sense at all. You would pay the full cost yourself and get nothing from insurance.

When full replacement changes the math

A full roof replacement in Georgia typically runs between $8,000 and $20,000 depending on size and materials. On a $400,000 home with a 2% wind/hail deductible, you owe $8,000 before insurance pays. If the replacement costs $15,000, insurance covers $7,000. That is worth filing. The table below illustrates how deductible type shifts the out-of-pocket picture:

| Scenario | Claim amount | Deductible type | Out-of-pocket | Insurance pays |

|---|---|---|---|---|

| Minor repair, flat deductible | $4,000 | $1,000 flat | $1,000 | $3,000 |

| Minor repair, 2% deductible on $350K home | $4,000 | $7,000 percentage | $4,000 | $0 |

| Full replacement, flat deductible | $16,000 | $1,500 flat | $1,500 | $14,500 |

| Full replacement, 2% deductible on $400K home | $16,000 | $8,000 percentage | $8,000 | $8,000 |

Wind/hail deductibles apply even for full replacements, which catches many homeowners off guard. They expect the percentage deductible applies only to small claims, but the trigger is the cause of damage, not the size of the claim.

Pro Tip: Installing hail-resistant roofing materials can reduce your deductible percentage and lower your premiums over time. Ask your insurer about discounts tied to impact-resistant shingles before your next roof replacement.

My take on roofing deductibles after years in this business

I have watched homeowners go from confident to completely blindsided the moment they learned their actual deductible. A couple files a claim after a bad hailstorm, expecting to pay $1,500 and move on. Then they find out their wind/hail deductible is 3% on a $380,000 home. That is $11,400 out of pocket. The look on their faces says everything.

In my experience, the homeowners who navigate claims best are the ones who read their policy every single year. Not just when they buy coverage. Every year. Coverage A limits change. Deductible percentages can be renegotiated. Installing better materials can shift your rates. These are not set-and-forget decisions.

I also see way too many homeowners trust contractors who promise to “handle” the deductible. I want to be direct: that arrangement almost always means inflated invoices. Your claim becomes fraudulent, and you are the policyholder on the hook. No short-term savings is worth that exposure.

The single best thing you can do right now is call your insurance agent and ask two questions. First, do I have a separate wind or hail deductible? Second, what is it in dollars based on my current Coverage A limit? Those two answers will tell you more about your real financial exposure than anything else in your policy.

— Dan

How Ir-ga helps you navigate roofing claims with confidence

At Ir-ga, we have worked with hundreds of North Georgia homeowners on storm damage claims since 2018. We know how confusing deductible language can be, and we believe every homeowner deserves honest, clear answers before work begins.

When you work with us, you get a licensed and insured roofing team that handles insurance claims transparently. We document damage accurately, communicate directly with adjusters, and never suggest inflating a claim to cover your deductible. If you are weighing repair vs. replacement options, we walk you through the real numbers so you can make the right call. Our step-by-step guide to storm damaged roof repair is also a great starting point if you have just experienced damage and are not sure where to begin. Reach out to Ir-ga today for a same-day response and a free, honest estimate.

FAQ

What is an insurance deductible for roofing?

A roofing insurance deductible is the amount you pay out of pocket before your insurer covers the rest of a roof damage claim. It is subtracted directly from your claim payout.

What is the difference between a flat and a percentage deductible for roofing?

A flat deductible is a fixed dollar amount, while a percentage deductible is calculated as a percentage of your home’s insured dwelling value, typically 1%–5%, which can result in thousands of dollars for wind or hail claims.

Do I have to pay a separate deductible for wind and hail damage?

Yes, in many policies, wind and hail damage triggers a separate percentage-based deductible that is higher than the standard flat deductible, even if the repair scope is similar to other covered claims.

Can a roofing contractor pay my deductible for me?

No. In many states, including Texas, it is illegal for roofing contractors to pay or waive your deductible. Doing so can result in claim denial and potential insurance fraud charges.

How do I find my roofing deductible amount?

Check the declarations page of your homeowners insurance policy. It lists your standard deductible and any separate wind or hail deductible, either as a dollar amount or a percentage of your Coverage A dwelling limit.