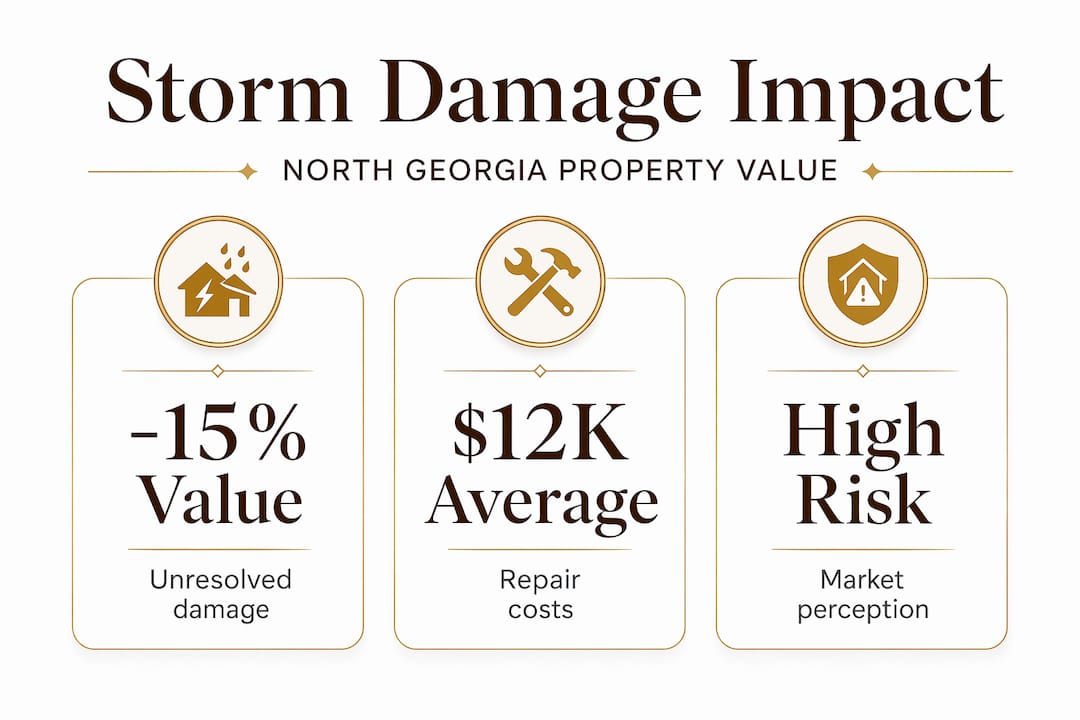

A lot of North Georgia homeowners assume that once the visible damage is repaired, their property value bounces right back. That assumption is costing people real money. Understanding how storm damage affects property value goes much deeper than patching shingles or repainting siding. The true impact involves repair quality, documentation, hidden moisture damage, and how buyers and appraisers perceive risk long after the storm has passed. Whether you own a home in Cherokee County or you’re an investor with properties across the greater Atlanta corridor, what you don’t know about post-storm valuation can significantly hurt your bottom line.

Table of Contents

- Key Takeaways

- How storm damage affects property value: the appraiser’s view

- Water intrusion and its long-term effect on value

- Why documentation and storm damage inspection matter

- Market dynamics, buyer behavior, and insurance costs

- Practical strategies to protect and restore your property value

- My take on what actually drives value loss after storms

- Restore your home’s value with Ir-ga’s storm damage expertise

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Appraisers look beyond surface repairs | Safety, structural soundness, and repair quality all factor into condition ratings and final appraised value. |

| Water damage is the silent value killer | Unresolved moisture from even minor leaks can trigger mold, rot, and system failures that deter buyers. |

| Documentation protects your value | Time-stamped photos, moisture readings, and repair records support claims and build buyer confidence. |

| Insurance costs reshape market demand | Higher premiums and coverage difficulty reduce buyer demand, suppressing property values even on repaired homes. |

| Licensed repairs preserve financing eligibility | Unpermitted or low-quality work lowers condition grades, making homes harder to finance and sell. |

How storm damage affects property value: the appraiser’s view

Most people think of a home appraisal as a simple comparison to nearby sales. After storm damage, it becomes much more detailed. Appraisers assess storm-damaged homes based on safety, soundness, sanitation, and the quality of repairs rather than just visible fixes. That distinction matters enormously.

The appraisal framework most lenders use is the Fannie Mae condition rating scale, which runs from C1 (new construction) to C6 (severe deterioration). A home that looks freshly painted but has structural issues from a storm, or repairs done without permits, can easily drop to a C4 or C5 rating. That lower rating doesn’t just affect appraised value. It can disqualify the home from conventional financing entirely, shrinking your pool of potential buyers to cash purchasers only.

FEMA housing inspectors evaluate storm-damaged properties using a similar lens, checking whether electrical systems, plumbing, and structural components are safe and livable. This approach mirrors what appraisers and lenders expect to see documented before they’ll place full value on a repaired property.

Here’s what appraisers and buyers focus on after a storm:

- Structural integrity: Roof deck, load-bearing walls, and foundation showing no signs of compromise

- Repair permits: Work completed without permits signals risk and can trigger condition downgrades

- Workmanship quality: Visible signs of rushed or mismatched repairs lower buyer confidence

- System functionality: HVAC, electrical, and plumbing must be fully operational with no storm-related damage

- Residual risk: Any indication of unresolved water intrusion or ongoing deterioration

Pro Tip: Before listing a storm-damaged property, ask your contractor to provide written confirmation that all work was permitted and passed inspection. That single document can protect your Fannie Mae condition rating and keep your buyer’s lender from flagging the appraisal.

Water intrusion and its long-term effect on value

Of all the ways storms reduce home value, water intrusion is the most destructive and the most underestimated. A small roof breach during a North Georgia hailstorm or high-wind event might not look like much from the street. Inside your attic or walls, though, the damage compounds quickly.

Water intrusion from storm damage causes wood rot, staining, mold, and system failures that lower property value over time. Mold can begin growing within 24 to 48 hours of moisture exposure. Once it spreads into insulation, framing, or HVAC ductwork, remediation costs escalate fast and buyers back away even faster.

The challenge for North Georgia homeowners is that our region’s humidity accelerates this process. A roof leak that might stay dry in an arid climate becomes a mold problem within days here during summer months.

Watch for these signs that hidden water damage may be affecting your home’s value:

- Staining or discoloration on ceilings and walls, even if dry to the touch

- Soft spots in flooring, particularly near exterior walls

- Musty odors that appear after rain or humid weather

- Peeling paint or bubbling drywall near windows and rooflines

- Unexplained spikes in HVAC repair needs

Ongoing moisture leads to costly repairs and directly reduces buyer confidence when it goes unresolved. The property value impact is not just about repair costs. It’s about perception. Buyers who see any sign of moisture history will price in worst-case scenarios, often discounting far more than the actual remediation would cost.

Pro Tip: After any storm event, get a moisture reading from a licensed contractor or inspector, even if you see no visible damage. Catching a 12% moisture reading in your roof deck before it becomes rot can save you thousands in value loss down the road.

Why documentation and storm damage inspection matter

Here’s a scenario that plays out regularly in North Georgia. A homeowner files an insurance claim after a storm. The adjuster arrives, spends 20 minutes on the property, and issues a settlement that covers cosmetic repairs but misses structural damage. The homeowner accepts the check, makes partial repairs, and later discovers at sale time that the appraisal flags unresolved issues. The claim window has closed. The documentation is gone.

A detailed, time-stamped storm damage assessment improves both repair quality and insurance claim outcomes. Comprehensive documentation includes room-by-room photos, moisture readings, and itemized damage lists that give you leverage against insurer underpayment and provide future buyers with confidence.

Compare what weak documentation versus thorough documentation produces:

| Documentation Type | Insurance Outcome | Appraisal Outcome | Buyer Confidence |

|---|---|---|---|

| Rushed adjuster inspection only | Undervalued claim, partial repairs | Lower condition rating possible | Reduced. Unanswered questions remain |

| Detailed room-by-room with photos | Accurate claim, full repairs funded | Supports higher condition rating | Strong. Repair history is verifiable |

| Moisture readings included | Hidden damage identified and covered | System integrity confirmed | High. No residual risk concerns |

Here’s how to document storm damage properly as a North Georgia homeowner:

- Photograph everything immediately after the storm, including the roof, gutters, siding, windows, and all interior rooms for any water entry points.

- Record moisture readings in attic spaces, wall cavities near roof penetrations, and any room below the roofline.

- List every item of damage room by room, including minor cosmetic issues. Adjusters often use incomplete lists to justify lower payouts.

- Save all contractor estimates and repair invoices, particularly those showing permit numbers and inspection sign-offs.

- Keep a timeline of when damage occurred, when repairs were made, and when inspections took place.

This documentation directly supports your insurance claim process and protects the house value post storm damage when it’s time to sell or refinance.

Market dynamics, buyer behavior, and insurance costs

Repairing a storm-damaged home is only part of the value recovery equation. How the market perceives your property after repairs is equally important, and that perception is shaped by factors outside your direct control.

Buyers price storm-damaged homes by weighing structural versus cosmetic damage, location, comparable sales, and repair estimates. Even a well-repaired home can sit on the market longer or sell below asking price if buyers associate the address with storm risk. In North Georgia, where severe hail and wind events are increasingly common, that risk premium is real.

Insurance costs compound the problem. Properties with storm damage history often see premium increases of 20% or more at renewal. Some carriers exit specific zip codes entirely after high-loss storm seasons. AI-driven property data now shifts modeled storm loss and insurance risk pricing by more than 15% for many properties. Homes with older roofs or unresolved vulnerabilities get priced at a higher risk tier, which directly increases carrying costs for buyers and narrows the qualified buyer pool.

Here is how the market dynamics play out for North Georgia properties post-storm:

- Buyer hesitancy: Even after full repairs, some buyers discount properties with a known storm damage history, particularly if documentation is thin

- Insurance premium increases: Higher premiums reduce affordability and suppress what buyers are willing to pay

- Coverage availability: In high-loss areas, finding adequate insurance becomes harder, further cooling demand

- Risk profiling technology: Storm-related risk data influences insurance pricing, which shapes how lenders and buyers assess long-term ownership cost

- Upgrades as value protection: Homes with impact-rated roofing, reinforced windows, or documented resilience upgrades can offset risk premiums and attract buyers willing to pay more

The good news is that targeted improvements, particularly a new roof installed by a licensed roofing contractor, can materially improve how both insurers and buyers categorize your property’s risk profile.

Practical strategies to protect and restore your property value

Taking the right steps after storm damage is not complicated. It requires consistency and attention to detail. Here’s what works for North Georgia homeowners and investors looking to protect their position:

- Use only licensed, insured contractors for all storm damage repairs. Unpermitted work is a red flag for appraisers and lenders, and it can void your homeowner’s insurance coverage on future claims.

- Maintain a complete repair file that includes photos, moisture readings before and after repairs, invoices, and permit numbers. Buyers and their agents will ask for this.

- Disclose damage history honestly when selling. Buyers who discover undisclosed storm damage after closing can pursue legal remedies. Transparency builds trust and supports your asking price.

- Consider stormproofing upgrades such as impact-resistant shingles or reinforced roof decking. These improvements can reduce insurance premiums and improve your property’s risk rating.

- Act fast after any storm event. The longer water intrusion sits unaddressed, the more expensive and value-damaging the secondary effects become.

Pro Tip: Investors should treat storm damage documentation the same way they treat title work: non-negotiable and worth every dollar. A property with a clean, verifiable repair history commands a premium over an identical home with a vague or incomplete damage record.

Reviewing a step-by-step guide to repairing storm-damaged roofs can help you understand exactly what quality repairs should involve before you hire anyone.

My take on what actually drives value loss after storms

I’ve reviewed enough storm-damaged properties across North Georgia to tell you that most of the value loss I see is entirely preventable. It doesn’t come from the storm itself. It comes from the decisions made in the 30 days after the storm.

The biggest mistake I see repeatedly is homeowners accepting the first insurance settlement without a thorough, independent inspection. Insurance adjusters are not bad actors, but they’re working fast and covering a lot of properties after a major weather event. Buyers demand transparency on storm damage history and quality of repairs, and a rushed settlement often funds repairs that satisfy the eye but not the appraiser.

I’ve seen homes lose $15,000 to $25,000 in appraised value not because of the original storm damage, but because of poor documentation and contractor shortcuts. The appraiser walks in, sees mismatched shingles, no permit pulled, and moisture in the attic. That combination signals a property that wasn’t properly restored, and the market prices it accordingly.

My advice is to think like an appraiser from day one. Would a professional looking at your repair record see a property that was properly restored? If you can answer yes with documentation to back it up, you’ve protected your value. If you’re not sure, the time to fix that is now, not at closing.

— Dan

Restore your home’s value with Ir-ga’s storm damage expertise

If your North Georgia home has taken storm damage, getting the repairs right the first time is the most important investment you can make in your property’s future value.

At Ir-ga, we specialize in storm damage repair across North Georgia, from Cherokee and Paulding counties to Cobb and Bartow. Our licensed and insured team handles everything from the initial damage assessment to full roof replacement, with comprehensive documentation built into every job. We also provide hands-on storm damage claim support to help you get maximum coverage without the guesswork. We’ve helped hundreds of North Georgia homeowners and investors recover full property value after storms. We’d like to do the same for you.

FAQ

How much can storm damage lower a home’s value?

Storm damage can reduce a home’s sale price by the full estimated repair cost plus an additional discount for perceived ongoing risk. Buyers factor in structural damage severity, repair quality, and comparable sales when determining their offer.

Does a storm damage history affect future appraisals?

Yes. If repairs were done without permits or with poor workmanship, appraisers may lower the condition rating, which reduces appraised value and can affect financing eligibility even years after the event.

What does a storm damage inspection cover?

A thorough storm damage inspection covers roofing, exterior cladding, windows, gutters, and interior moisture levels. Comprehensive documentation includes room-by-room photos, moisture readings, and an itemized damage list to support both repairs and insurance claims.

Can storm-resistant upgrades increase property value?

Yes. Homes with impact-resistant roofing and documented resilience features benefit from lower insurance risk ratings. AI-driven risk models now factor in roof age and construction quality, which can lower premiums and improve a property’s appeal to buyers.

How soon should I document storm damage after a weather event?

Document damage immediately, ideally within 24 hours. Quick documentation before any cleanup captures the full scope of the event and strengthens your insurance claim. Delays allow secondary damage to develop, complicating the claim and raising the cost of restoring full property value.